AMAG Austria Metall AG: Road to success continued in Q3 2022

- Significant revenue growth of 47 % to EUR 1,353.9 million (Q1-Q3/2021: EUR 923.8 million)

- EBITDA grows by 48 % to reach an all-time high of EUR 217.4 million (Q1-Q3/2021: EUR 146.5 million)

- Significant growth in net income after taxes of 87 % to reach EUR 106.7 million (Q1-Q3/2021: EUR 57.0 million)

- Optimised product mix and very good use of existing plant and personnel capacities as well as stable production play a crucial role

- Further business performance is being increasingly affected by partially declining demand and a general slowdown in the market as well as by high energy prices

- Outlook for 2022: EBITDA between EUR 230 million and EUR 250 million based on current estimates for trends in shipment volumes and prices, and assuming stable energy supplies

- Continued solid growth expectation for aluminium products in the medium and long term*

*See CRU Aluminium Market Outlook, October 2022

AMAG Group achieved further year-on-year growth in revenue and earnings in the first three quarters of the year. This was the first time in the company’s history that an operating result (EBITDA) of over EUR 200 million was generated. Thanks to sustained high productivity, continuous product mix optimisation as well as the good use of existing capacities, AMAG has successfully leveraged the predominantly positive market environment. Tailwinds also came from the interest that AMAG holds in the Canadian smelter Alouette, which benefited from attractive aluminium and raw material prices accompanied by solid production levels.

Gerald Mayer, CEO of AMAG Austria Metall AG, comments: “Despite numerous challenges, we have achieved the best operating result in the company’s history. With our innovative and sustainable products as well as a clear focus on sustainable production, we made the best possible use of the positive market environment. However, the course of business going forward is characterised by uncertainties. We will continue to make the best possible use of our broad positioning and respond flexibly to changes in demand.”

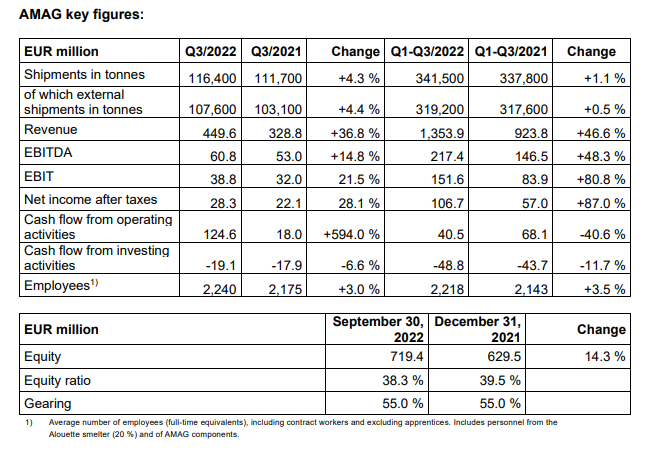

AMAG Group revenue posted considerable growth of 46.6 % to EUR 1,353.9 million in the first three quarters of 2022 (Q1-Q3/2021: EUR 923.8 million), mainly reflecting the higher aluminium price level, price adjustments due to increased costs, and optimisation of the product mix. The significantly weaker EUR against the USD also exerted a revenue-enhancing effect. At 341,500 tonnes, total shipments were slightly above the previous year’s level (Q1-Q3/2021: 337,800 tonnes).

Earnings before interest, tax, depreciation and amortization (EBITDA) grew significantly by 48.3 % to reach EUR 217.4 million (Q1-Q3/2021: EUR 146.5 million). With production levels remaining solid, the Metal Division benefited from the attractive average aluminium price and relatively favourable alumina costs. The Casting and Rolling divisions were characterised by high productivity as well es by an optimised use of existing capacities. The successful implementation of product mix optimisations and price adjustments to reflect higher costs for primary materials and energy also exerted a positive effect.

Taking into account depreciation and amortization of EUR 65.7 million (Q1-Q3/2021: EUR 62.7 million), the operating result (EBIT) also increased considerably to EUR 151.6 million in the reporting period (Q1-Q3/2021: EUR 83.9 million).

Net income after taxes almost doubled year-on-year to EUR 106.7 million in the first nine months of the year (Q1-Q3/2021: EUR 57.0 million).

As expected, cash flow from operating activities at EUR 124.6 million recorded a very positive trend in the third quarter of 2022. Overall, the cash flow from operating activities after nine months amounted to EUR 40.5 million (Q1-Q3/2021: EUR 68.1 million). The high level of earnings has a positive impact, while higher raw material prices and inventories, in particular, increase capital employed and thereby exert the opposite effect.

A total of EUR 48.8 million was spent on investments in the first nine months of this year (Q1-Q3/2021: EUR 43.7 million). Accordingly, free cash flow amounted to

EUR -8.3 million in the period under review (Q1-Q3/2021: EUR 24.4 million).

Net financial debt stood at EUR 395.8 million as of September 30, 2022, compared with EUR 346.1 million as of the end of the 2021 financial year. Equity grew from EUR 629.5 million at the end of 2021 to EUR 719.4 million as of the current quarterly reporting date. At 38.3 %, the equity ratio remained at a stable level, compared to the end of the year 2021 (December 31, 2021: 39.5 %).

Earnings trends in the third quarter of 2022

Total shipments increased significantly to 116,400 tonnes in the third quarter of 2022 (Q3/2021: 111,700 tonnes). The average aluminium price decreased quarter-on-quarter from 2,654 USD/tonne to 2,358 USD /tonne. A positive change arose in premium income for primary aluminium deliveries. At the AMAG site in Ranshofen, especially price adjustments to reflect higher costs had a positive impact on AMAG Group revenue. Overall, the quarter under review thereby recorded an increase of 36.8 % to EUR 449.6 million (Q3/2021: EUR 328.8 million).

EBITDA increased significantly from EUR 53.0 million in the previous year to EUR 60.8 million in the period under review, which especially reflects solid production levels at the Canadian subsidiary Alouette as well as high productivity and successful optimisations in the product mix. To date, increases in raw material and energy costs have been largely offset by price adjustments.

Taking into account depreciation and amortization of EUR 22.0 million (Q3/2021: EUR 21.0 million), AMAG Group also reported significant growth in EBIT to EUR 38.8 million in the past quarter (Q3/2021: EUR 32.0 million). At EUR 28.3 million, net income after taxes in the quarter under review reflects the positive performance during the quarter (Q3/2021: EUR 22.1 million). As expected, a particularly high level of cash flow from operating activities of EUR 124.6 million was generated in the third quarter of 2022.

Outlook for 2022:

To date, the financial year has been characterised predominantly by a positive market environment. However, the economic environment increasingly slowed during the course of the third quarter of 2022, mainly reflecting uncertainties in connection with the Ukraine war and considerable cost inflation, primarily due to rising energy prices. Moreover, uncertainty surrounding the continuity of energy supplies remains.

Although existing energy price hedges and the broad product portfolio cushion the related impact, AMAG Group expects an increasing effect on earnings due to rising costs and declining market expectations in general. This development is also partly reflected in the new incoming orders from individual customer industries. According to the Commodity Research Unit, general growth expectations for aluminium products remain solid in the medium and long term.*

Based on current estimates for trends in shipment volumes and prices, and assuming stable energy supplies, the AMAG Management Board anticipates EBITDA between EUR 230 million and EUR 250 million for the full 2022 financial year.

*See CRU Aluminium Market Outlook, October 2022